KYC: A modern approach incorporating AI, biometrics and more

Contents

This complete picture is critically important due to the rapid adoption of digital payments, online banking, neo-banks and other FinTech applications—especially in emerging economies. For example, Statista research shows that more than 415 million people in Latin America and the Caribbean regularly use FinTech tools. In African nations, the electronic payments market is growing at a rate of 20% annually, according to the Center for Strategic & International Studies (CSIS).

This article will examine how companies employ a modern approach to identity verification, the keys to streamlining the KYC process and how to choose a KYC vendor to leverage emerging technology.

What is KYC?

KYC is the mandatory practice of identifying and verifying a customer’s identity for financial institutions. When opening an account—and periodically throughout the relationship—financial institutions must:

- Conduct risk assessments

- Implement customer identification and verification procedures

- Establish customer due diligence procedures

- Ensure ongoing monitoring and record keeping

KYC technology is not just about fulfilling compliance obligations; it also enhances the user experience by reducing user friction during the identity verification process.

Simplifying the process is crucial in welcoming new customers. They expect a quick and smooth verification that works instantly, especially online

Reducing friction in the process is crucial, especially when onboarding new customers. Customers now expect a streamlined and efficient verification process that works nearly instantly, especially when conducting business online. Business and merchant customers also expect the highest levels of data security, transparency on how data is collected and used, and minimal disruption to their banking experience.

The information gathered in a modern KYC process helps create a more complete picture of individual customers. Today’s identity verification process leverages technology and automation in various ways. So, let’s examine the elements that make up a modern KYC process.

What elements are part of modern KYC?

While traditional KYC remains a manual process, including physical copies of identification documents and manual checks, eKYC leverages electronic tools to verify customer identities, pulling in a wider variety of data and signals than traditional KYC. Customers submit documentation electronically, and the verification process is automated. Customer information is compared to known databases and resources to verify identity, including third-party data, passive signals, and behavioral data. eKYC increases processing speed, accuracy, and scalability without sacrificing privacy.

Here are some ways eKYC leverages technology to improve the identity verification process:

Artificial intelligence and machine learning

AI and ML automate much of the KYC process, analyzing customer documentation with reference databases and looking for matches and discrepancies. This process is faster and more reliable. Manual reviews produce significant false positives, but AI can reduce false positives by as much as 70%.

Optical character recognition (OCR) can extract and process data from ID documents, comparing them to existing databases. Data analytics can detect patterns or anomalies that provide indicators of risk or fraud, improving the effectiveness of the verification pattern.

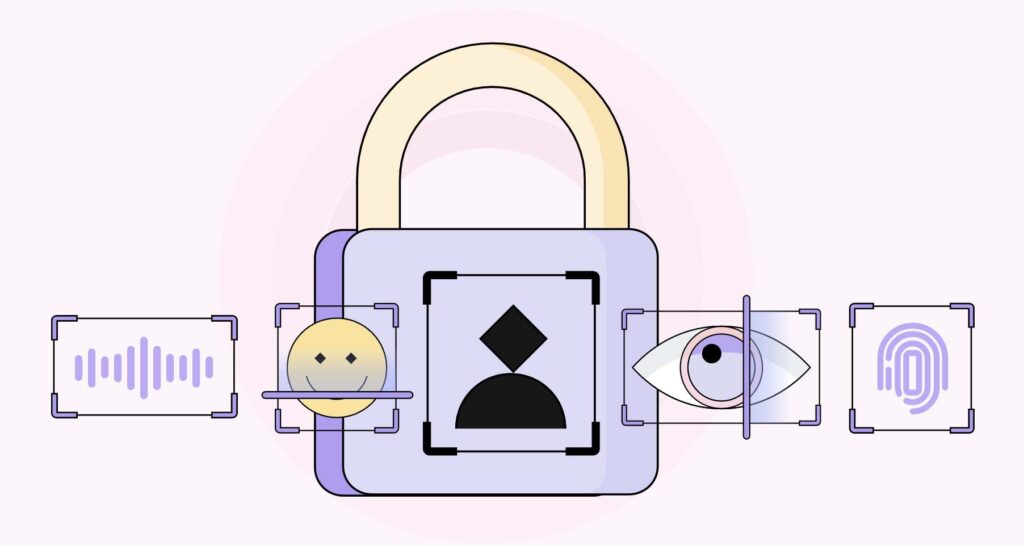

Biometric identification

eKYC leverages biometric identification to verify identity by capturing fingerprints, iris scans, facial recognition, or voice matching. Comparing data to existing biometric databases can verify identities with a high level of confidence. Unlike physical documents that can be altered, biometric data is significantly more difficult to fake.

Biometric identification is becoming more widespread. For example, more than 1.3 billion residents in India have signed up for Aadharr, India’s national biometric electronic ID. Japan, South Africa, Nigeria, Brazil and other countries have seen significant deployment of biometric ATMs using fingerprint and finger vein recognition for identity matching. The biometric ATM market is growing at a compound annual growth rate (CAGR) of nearly 40% and is expected to reach US $42.59 billion by 2029.

Scalability and compatibility with existing systems

AI also enables scalability to accommodate large volumes of customer data and transactions without compromising security. Modern eKYC solutions can integrate with existing banking systems and infrastructure to streamline workflow and create significant efficiencies.

The most complete picture of a customer possible

KYC is evolving beyond basic identification and verification, providing a more complete picture of customers. This comprehensive picture can help identify patterns, find anomalies, and predict future behavior.

How does modern KYC create a fuller picture? There are several components:

1. Access to many data resources

Multiple data sources can also help reduce false positives and improve accuracy and efficiency. Today, businesses can access a wide variety of data sources, including:

- Credit reports

- Public records

- Accessible government databases

- Social media

- Third-party data providers

With access to various sources, organizations can more accurately validate customer identities, assess financial risk and remain compliant with anti-money laundering (AML) regulations. More sources provide a more complete picture, helping proactively identify suspicious activity and reduce fraud.

With access to different sources, organizations can better confirm customer identities, evaluate financial risks, and follow anti-money laundering (AML) rules. Having more sources gives a clearer picture, helping spot suspicious activity early and preventing fraud.

For example:

- Financial institutions can verify customer names, addresses, and other personal information using public databases and internal records.

- Available credit reports in most countries can help evaluate creditworthiness and payment history to establish risk parameters.

- Social media reviews can reveal additional information about customer backgrounds and connections.

By leveraging diverse data sources, companies can build a more comprehensive view of their customers and make better-informed decisions. Modern KYC goes beyond assessing risk in general, helping companies to understand where and why they are facing high risk so that companies can be more confident in approving users that might have previously been rejected.

With eKYC, you have the flexibility to use multiple sources to fit your risk tolerance levels and meet all compliance regulations.

Identity verification requires users to pass Tier 1 KYC requirements by ensuring identities match government ID verification with government databases. Technology can be employed to allow users to pass Tier 2 KYC by taking a selfie and verifying users using liveness detection. Tier 3 KYC verification can use location intelligence and additional documentation to verify address and location. Finally, AML verification can compare documentation against AML watchlists to comply with KYC requirements.

Access to more data resources also expands the use of KYC tools. For example, you can use credit checks, bank and credit card data, and customer behavior to assess financial risk and qualify customers for loans automatically.

2. The ability to include or exclude different data fields

Including or excluding data fields can streamline the identity verification process for KYC users. Limiting required information to only what’s necessary and relevant reduces friction and eliminates steps in the KYC process.

Besides being more efficient, this also requires collecting, processing and storing less data, reducing the risk of privacy violations and jurisdictional data compliance.

For example, a FinTech provider that offers credit card services may only need a customer’s name, address and national ID number to verify identity. A bank offering investment services may require additional information, such as tax identification numbers (TINs), income sources and verification, and employment details.

Customizing data collection, workflows and adding or deleting data fields based on business needs creates a better user experience and makes the entire process more efficient for everyone. A seamless and frictionless process helps build trust with customers when the KYC process is more relevant and personalized to user requests. This increases the odds users will complete the process.

3. Building richer profiles of individuals over time

Improving the accuracy and efficiency of KYC requires building deeper and richer profiles of customers. As more data is added, companies can build a more comprehensive picture to help accurately verify identities and assess potential risks.

Enhancing KYC effectiveness means creating detailed customer profiles that are accurate and efficient. As more data comes in from various sources, user profiles become even more valuable, creating a network effect that enriches the overall understanding.

As additional data is gathered from related parties, the network effect comes into play, making the user profiles richer. For example, a bank that services multiple product lines for its customers can combine data from credit card transactions, loan applications and savings accounts to build a more comprehensive profile.

AI and machine learning can use additional data to better identify potential risks or fraudulent account activity. By analyzing historical data and similar user behavior, algorithms can identify potential opportunities to expand services or identify specific risks that are likely to develop. These rich profiles can also help produce a deeper and more personalized customer relationship, helping with retention and loyalty.

These deep insights into customers further reduce fraud and identify suspicious activity.

4. Customizable risk scoring

Instead of a straightforward accept or reject, customizable risk scoring enables a more granular approach that can be applied to individual users. Due diligence and monitoring can be tailored based on individual behaviors and emerging threats.

Customizable risk scoring can deploy automation to assess a wide range of factors, including:

- Risks: These can include geographical locations, transaction amounts and volumes, funding sources and association with politically exposed persons (PEPs).

- Weighting: Financial institutions can assign different weighting and parameters based on current regulatory environments, emerging threats and corporate risk profiles.

- Scoring: Scoring can also be customized based on a combination of qualitative and quantitative criteria.

- Triggers: Financial institutions can define thresholds and triggers for different classes of users. For example, high-risk customers may trigger enhanced due diligence.

Just as importantly, good software needs to provide an auditable trail of what decisions were made and why to allow humans to check and potentially change those decisions. This is especially true in the era of AI. So, automation is crucial, but auditability is just as important.

Customizable risk scoring enables greater flexibility to adapt to evolving risks, changing regulatory environments and internal risk assessments. This flexibility also includes the ability to adjust weighting or make different decisions based on changing criteria or risk tolerance levels.

Where security and privacy fit in when choosing a KYC vendor

Regardless of whether companies use traditional KYC or modern eKYC tools, security and privacy are essential to meet regulatory compliance and protect customer assets. Take the example of South Africa’s Postbank, which had to replace 12 million bank cards after the compromise of the personal data of millions of customers. This cybercrime affected some 10 million customers, resulting in 25,000 fraudulent transactions and the theft of R90 million from accounts.

As cyberattacks aimed at financial institutions continue to increase, a recent IMF survey across 51 countries detailed significant security gaps that require stronger solutions.

When choosing a KYC vendor, you must understand the measures taken to ensure data security. This includes collecting, storing and processing sensitive user data, along with compliance with international privacy regulations. When working with any third-party provider, you must do your due diligence to be assured they meet your rigid compliance standards.

Security certifications

Ask for independent, third-party security certifications. Certification objectively validates the vendor’s commitment to maintaining robust security measures and demonstrates that a vendor has undergone rigorous assessments and audits. This ensures their systems and processes meet established industry standards.

Security certifications such as ISO 27001 (Information Security Management System) or SOC 2 (Service Organization Control) assure that the vendor has implemented appropriate safeguards to protect user data from unauthorized access, breaches, and data loss. Moreover, security certifications can be vital for regulatory compliance. Many industries, such as finance and healthcare, are subject to strict data protection regulations. By obtaining security certifications, a KYC vendor can demonstrate their commitment to meeting these regulatory requirements and provide evidence of their compliance posture.

Security certifications are tangible evidence of a KYC vendor’s dedication to maintaining the highest standards of security, instilling trust, ensuring regulatory compliance, and protecting sensitive user information.

How to choose a KYC partner

Choosing a KYC partner is a significant decision, so you want to make an informed decision. You will want to evaluate potential identity verification providers in several ways:

- Identify specific requirements

You will want to identify any specific requirements or capabilities you need, such as the desired level of automation, risk tolerances, geographical compliance and future growth plans. You must ensure your KYC solution will work in whatever jurisdictions you plan to do business with. Your requirements should also include the ability to get the most complete picture possible.

- Technical assessment

Your KYC solutions must accommodate your workflow seamlessly and integrate with your existing systems. Ensure any KYC software provider can handle your anticipated volume and allows for scalable options for future growth. You will also want to ensure that any KYC provider you work with employs modern technology to leverage AI and ML to provide a more complete picture of customers.

- Security assessment

You must also evaluate any vendor’s security and ensure they align with your organizational requirements. Assess regulatory frameworks and ensure they meet industry and geographical compliance.

- Confirm legal and compliance

Make sure your KYC provider meets your organization’s legal and compliance measures. You want to make sure your internal legal teams (or external legal teams) sign off on your KYC solution and validate its effectiveness in meeting your legal and regulatory compliance obligations.

- Try a free version and determine proof of concept

As part of your due diligence, you will want to get product demos and try a free version of the software solution to ensure it works within your workflow. Or run a proof of concept to ensure compatibility. Talking to a consultant from your KYC vendor can help you better assess your existing tech stack and how their software can integrate.

- Work with modern KYC experts

You must choose a KYC solution that meets both compliance standards and enables the flexibility you need to customize the solution to your specific risk tolerance and workflow. Talk to experts, such as the KYC consultants at Metamap.

You also want to make sure that your provider offers extensive training, enabling you to use the platform to its fullest.

How Metamap helps solves KYC challenges

We believe you’ll find MetaMap to be the most complete customer identity platform. MetaMap empowers businesses so that they can more accurately understand the audience with whom they want to transact. We source and integrate a vast range of user data into a single platform to get a more complete picture of your users.

Our automated and AI-powered identity verification solutions enable businesses to gain a deeper understanding of their users, get instant access to users’ bank account transaction history and income, verify ID ownership, and prevent fraud while remaining compliant with local and global regulations.

Our clients can create their own verification flows to fit their needs with a simple drag-and-drop builder or choose from our ready-to-use templates. Our platform is easy to deploy and requires no coding.

MetaMap gives you the power to reach more people with more products and services than ever before.

Learn more about MetaMap. Book a call.

Related content

Subscribe to the newsletter and stay up to date with promotions, special offers and news